DeFi: Building a New Financial System

Decentralised Finance and the opportunities.

The last 6 months have been kind of a test for humanity. The world was shook and the status quo has changed from one day to another. What’s left now is economic uncertainty and the recurring question: “What is the new normal?”

More and more people seem to arrive at the conclusion that we need to work out new policies in order to endure & survive. These policies should be implemented on a global, regional and a national scale to make sure we are ready for other challenges. All the efforts are important, but arriving at agreements can be very difficult.

There is a saying: “With great change comes great opportunity.” We believe that alternatives and improvements can be facilitated by radical concepts and visions.

One of them is Decentralised Finance.

🌐 What is Decentralised Finance?

Decentralised Finance (DeFi) is one of many use-cases of cryptocurrency. It allows investors, holders, lenders, borrowers, alike to hold, trade and transact digital assets. DeFi aims to re-create our traditional financial system and is one domain of the crypto space which has traction and could reach adoption on a global scale. One could simply look at DeFi as the most recent breakthrough in Fin-Tech, but there is more…

This new financial universe is powered by Blockchain, Cryptography, Web3 and the existing Internet. Bitcoin was the first global network to benefit from this tech-stack, it solves the problem of peer-to-peer payments and is considered “digital gold”.

Ethereum, the second biggest cryptocurrency, goes one step further. Ethereum is a Smart Contract Platform, which means the network can include a more complex logic to the applications living on the blockchain. This opens the floor for a variety of completely new, programmable digital assets.

💡Ethereum is a pure software system where the code enforces the state of a contract, and not a third party institution relying on a pen and paper legal contract.

Thanks to this technological advantage and other network effects, first DeFi protocols spawned on Ethereum and gained attention throughout 2018 and 2019. Since the drop of stock prices, increasing inflation and decreased global economic activity in the beginning of 2020 many people started looking for alternative saving and investment opportunities. DeFi may provide options to hedge against the looming financial crisis.

The crypto markets facilitating these interactions and products are still small compared to our legacy banking system and even though hundreds of millions steadily flow into DeFi every week, the ecosystem is full of blank spots and whitespaces to fill out. All these new applications still include certain risks, so one should have a basic understanding of the things going on, before interacting with these protocols.

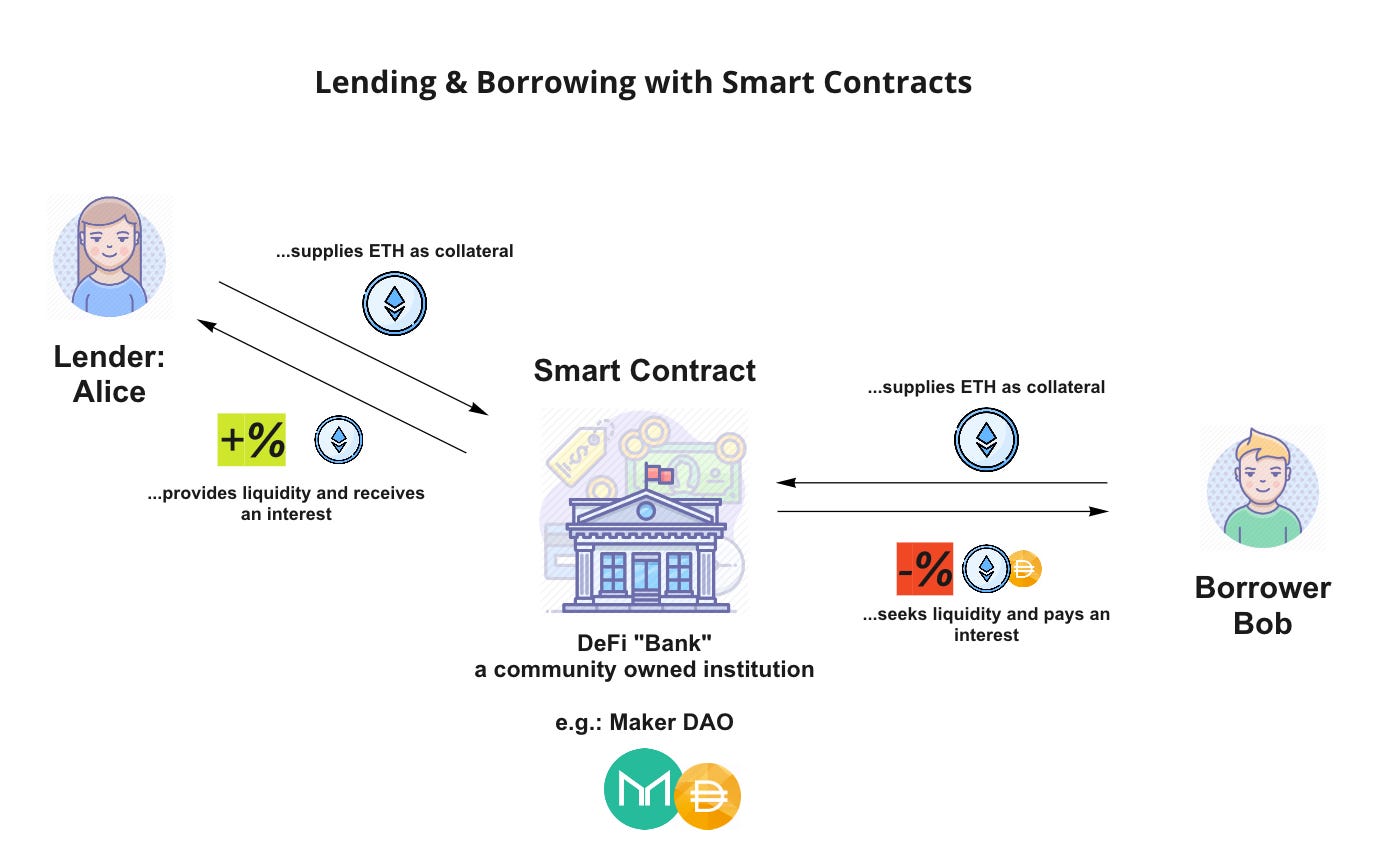

Let’s explore the most popular use-case of DeFi:

Lender Alice locks her tokens as a collateral in the decentralised finance protocol, a community-owned system of smart contracts.

Borrower Bob locks his collateral, to borrow digital assets within a certain safety margin. (All loans are over-collateralised)

Bob pays the interest for his debt to the protocol, which then distributes it among all lenders like Alice with every new block of the blockchain.

After Bob repaid his debt and the outstanding interest, he can exit his collateral immediately.

Alice keeps her assets locked and still receives interest from other borrowers using the smart contracts of the protocol.

✨ What is the Magic of DeFi?

DeFi started as a quest for economic freedom. It benefits from the underlying tamper-proof technology and covers many benefits of the traditional financial system.

All we have to rely on is the security of the blockchain, which is maintained by a global network of users, developers, projects and initiatives.

This new financial system is online and reality, in the sense that everybody can use these services, or create their own. There are no gatekeepers.

Global networks of people can pool capital and organise themselves efficiently to grow the amount of that capital and grow their abilities as a network.

The organisational structure of these networks is captured in code and enforced by software, not by a physical entity or third party.

Any two people in the world can enter a business agreement and start a company, which rules & incentives are managed by a smart contract.

The amount of capital flowing into DeFi protocols has broken the 1 Billion $ mark in May, since then the Total Value Locked has grown 500% (see graphic below).

image credit

It has only been 5 years since the first transaction on Ethereum in 2015. Hard to imagine what is happening in the next years with an exponential growth predicted within the cryto community, social networks & media … but let’s take a look:

🌄 What comes next?

{kind=link}

With such powerful technologies in place, the next big things on the horizon could be community owned money markets and payment networks, replacing centralised companies like VISA, MasterCard or PayPal.

Freelancers could build global worker cooperatives, Crowdfunding campaigns become peer-to-peer and transparent. Individuals and Families can maintain their savings and personal investments in a secure and frictionless way.

Think of incentive and funding systems, which reward users for not taking the car and reducing CO2 emissions, coordinating the preservation of local infrastructure and public goods like urban gardening or facilitating tool sharing platforms which work with the same collateral mechanisms as the lending protocols in DeFi.

We recognise Decentralised Governance is steadily emerging in favour of people-owned institutions with great network effects and a healthy and engaged community. That’s why we look excited into the future and provide the scaling and organisation solutions to make all this a reality!

👀 Thank you for reading, what’s your take on this?

Let us know on Twitter 🐦